Challenges in Business Succession Planning: Cash Flow Strategies for Estate Tax Liabilities

Tax Strategist Insight

Individuals with substantial business holdings often face complicated estate tax issues, the costs of which can be unexpected and significant. Failing to recognize and plan for these issues may adversely impact the ability of the estate to timely pay any estate tax it owes. What is more, a lack of planning can affect the ability of the business to continue operating in the manner envisioned by the current and succeeding owners. As the complexities vary by situation, having a tax efficient business succession plan geared toward maintaining a particular business as well as satisfying the owner’s specific intentions is key to helping preserve family wealth.

When developing a business succession plan, thought should be given to:

- When the business interests are best suited to be transferred;

- Who or what entity should receive the interests (or resulting distributions of income where, for example, the interests are held by a trust); and

- Whether the interests should be transferred by gift during the owner’s lifetime, sale during the owner’s lifetime, through the owner’s estate, or a combination of these methods.

Importantly, current and succeeding owners also should consider how to provide the cash flow needed to pay any estate tax due while continuing to operate the business. This article discusses some of the tax and cash flow planning strategies specific to estate taxes, as well as other issues and opportunities that may be addressed as part of a well-informed business succession plan.

Insight

Effectively transitioning a business to the next generation of owners through a business succession plan that incorporates estate tax planning will result in the most value being retained by the owners and their families. Whether the business is entirely family owned or has unrelated owners, each scenario comes with its own complications but with considerable overlap in planning opportunities. The business succession plan that will be most effective for the family and remaining business owners depends on many factors, including how ownership in the business is currently held, how the ownership is to be transferred, the type of industry, where the business sits in the business growth cycle, the value of the business, and available cash flow.

Lifetime Transfer Planning Opportunities

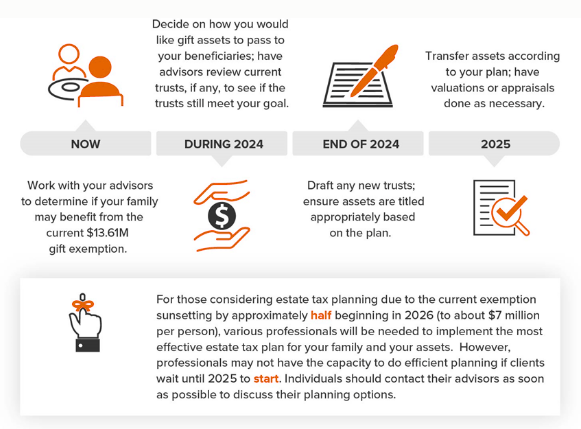

Current owners may wish to transfer some or all of their business interests to the next generation of owners during their lifetime, to allow themselves flexibility to exit the business gradually and provide a period of transition for their successors. For 2024, current law allows individuals to transfer free from gift and estate tax a historically high $13.61 million in assets through gifts during the transferor’s lifetime, through their estate, or through a combination of both.

However, beginning January 1, 2026, the estate and gift tax exemption will essentially be cut in half, leaving every dollar of value above the reduced exemption amount subject to federal gift or estate tax of 40% (certain states also have a gift or estate tax). This provides a potential planning opportunity for business owners to transfer assets and future asset growth out of their estate before 2026. Transfers may be outright to individuals or into a trust for the benefit of individuals and even for multiple generations, which may allow for additional estate tax savings for successive generations. While a trust owns the interests, there are trustees, investment advisors, and business managers that direct the ownership and management of the business interests to provide some restrictions on assets and distributions to beneficiaries. Because of the inherent complexities and time involved, consideration of this type of planning should begin sooner rather than later so that transfers may be implemented in the most effective manner.

Payment of Estate Tax — Installment and Deferral Options

Even with an optimized gifting plan for an owner’s business interests, in many cases there will still be estate taxes due after the owner’s death. There are a few options to pay the estate tax liability over time to help with cash flow issues of the estate and the business. These options, which generally avoid late payment penalties but accrue interest on amounts paid after the original due date, include:

- Electing to make installment payments of the estate tax associated with qualifying closely held business interests under Code Section 6166;

- An estate loan, where the interest on the loan may be deductible; and/or

- Submitting a request to the IRS for an extension of time to pay the estate tax under Code Section 6161.

Installment payments. To be eligible to make installment payments of estate tax under Section 6166, the adjusted gross estate must be composed at least 35% of closely held business interests as defined by the Internal Revenue Code. Section 6166 allows a maximum of 10 annual installments, with the option to begin paying the installments no later than five years after the original estate tax due date — thus allowing qualifying estates a total extended payment period of up to 14 years. Accrued interest is payable annually from the original due date. The deferral applies only to the amount of estate tax associated with the closely held business interests. Estate taxes not attributable to closely held businesses will still be due within nine months after the death of the decedent.

Section 6166 deferrals will cease and the associated estate tax and accrued interest will be accelerated if:

- Any portion of an interest in a qualifying closely held business is distributed, sold, exchanged, or otherwise disposed of, or property attributable to such an interest is withdrawn from the trade or business; and

- In the aggregate, such distributions, sales, exchanges or other dispositions and withdrawals equal or exceed 50% of the value of the closely held business.

Certain types of redemptions are not considered when applying this acceleration rule. An annual certification that an acceleration event has not occurred must be completed each year by the estate fiduciary. If acceleration is triggered, the IRS may place a lien on business interests or assets, and potentially other estate assets, until the estate tax and interest have been paid in full.

Estate loan. The use of an estate loan is another option. An estate loan can provide an estate the funds it needs to pay its estate tax when due, with the estate repaying the loan over time based on the terms of the loan agreement. The interest payable over the life of the loan may be deducted on the estate tax return, but only if all of the following conditions are met:

- The loan may not be prepaid;

- The interest is payable at a fixed rate;

- The estate is illiquid; and

- The deduction is allowed under the laws of the state where the estate is being administered.

Request for payment extension. Section 6161 allows the IRS discretion to grant an extension to pay the estate tax in certain situations. Under this Section, the IRS may grant, in one-year increments, a total extension of up to 10 years for reasonable cause that would lead to “undue hardship” for the estate. A Section 6161 extension is typically not relied on for planning purposes but may be a fallback if other payment deferral options are unavailable.

Funding the Estate Tax — Cash Flow Planning

Notwithstanding the ability to sometimes use installment payment options for estate tax, additional cash flow planning strategies may be considered to help ensure funds are available to pay the tax when due. Normally available options include the use of:

- Buy-sell agreements (which may be partially funded with life insurance);

- Life insurance arrangements; and/or

- Non-business assets.

Buy-sell agreements. A buy-sell agreement provides terms under which a business and/or its owners have the option or requirement to purchase another owner’s interest upon the occurrence of an event, usually including the death of the owner whose interest is purchased.

When a business is family owned, the business interests are typically gifted to family members and, therefore, buy-sell agreements are not frequently implemented. However, when buy-sell funding is anticipated, an important consideration is the determination of purchase price. The parties to a buy-sell transaction will be bound by the purchase price set out in the agreement but, under the tax law, the IRS may assert a different fair market value of the business for estate tax purposes. If the buy-sell agreement does not value the interest to be purchased reasonably in line with the IRS’s determination of fair market value, the proceeds received by the selling owner or their estate may be lower than the value upon which estate tax is assessed. To help avoid estate tax valuation disputes, buy-sell agreements should include a fair market value purchase price determined using tax principles, which is the value that a willing buyer and a willing seller would agree at arm’s length.

When drafting the buy-sell agreement, business owners and their advisors need to be cautious not to accelerate the estate tax due date by inadvertently terminating a Section 6166 installment payment election (see Installment payments, above). Otherwise, what might have been a 14-year deferral could be considerably shorter.

Buy-sell agreements may be partially funded with life insurance. A derivation of an insurance funded buy-sell agreement is a “cross purchase agreement,” where each owner holds a life insurance policy on other owners to be able to purchase business interests in the case of an owner’s death. Since cross purchase agreements require policies to be owned by each owner on all other owners who are part of the arrangement, this option may be best suited for businesses with only a few owners.

When buy-sell agreements are funded with life insurance held by the business as the beneficiary, it is important the arrangement is structured so that the insurance proceeds are not included in the value of the business for estate tax purposes upon the death of the owner. Otherwise, this type of arrangement can result in a higher estate tax value and, therefore, a higher estate tax liability associated with the business. When evaluating this issue, the IRS looks at factors to determine if a purchase agreement with life insurance funding is a bona fide business arrangement that is comparable to other negotiable arm’s length transactions, including whether the arrangement is in line with similar industry terms and whether the parties have abided by the terms of the agreement. Deviation from an agreement may impact the case to exclude the insurance from the value of the business and ultimately the amount of estate tax that may be payable.

On March 27, 2024, the United States Supreme Court heard oral arguments in Connelly v. United States, a case in which the U.S. Court of Appeals for the Eighth Circuit ruled that life insurance proceeds must be included in the estate tax value of a business and did not allow for an offsetting reduction in value for the requirement of the business to redeem shares from the shareholder’s estate. In Connelly, the buy-sell agreement terms were not followed for the purchase price to be paid for the shares, which had included an appraisal requirement, albeit without a fixed formula for establishing the redemption price.

Insight

To help avoid unintended and potentially costly complications, parties to a buy-sell agreement should ensure that all terms they agree to are followed, the agreement complies with the technical tax rules for valuing business interests for estate tax purposes, and the agreement’s terms are comparable to similar arm’s length arrangements. In addition, taxpayers should monitor the Supreme Court’s ruling in Connelly, which will shed additional light on using buy-sell agreements with life insurance funding in estate tax planning.

Life insurance arrangements. There are other opportunities to fund estate tax with life insurance. For families, this is sometimes done through the use of an irrevocable life insurance trust. For families as well as other owners, it may be through business owned life insurance, a business life insurance entity, or a cross purchase agreement. Life insurance usually does not cover the entire estate tax liability attributable to a high growth company; therefore, installment payments should be considered in conjunction with this option.

Non-business assets. The business or the estate may hold assets that are not needed for business operations, such as money market accounts or other non-business assets or investments. Where possible, these assets could be liquidated to help fund the estate tax.

Equalizing Gifts of Interests in Family Businesses

An important consideration for family businesses is the owner’s wishes regarding equalization of gifts to children. Interests in family businesses are commonly transferred by gift or trust to surviving family members, either equally or only to those involved in the business operations. Business governance and setting beneficiary expectations are essential to help avoid or reduce potential family discord over how the business is managed and the planned succession of ownership.

For example, when one child works in the business but their siblings do not, issues can arise over how the owner wants the business to be transferred among the children. Business owners may want the interests:

- Transferred equally among all of their children;

- Transferred only to the child that works in the business, with other assets of equal value transferred to the siblings; or

- Transferred to one or more children with no equalization.

In addition, rights of first refusal may be granted so that the children that work in the business may buy out the interests of their siblings. Business owners should work with their advisors to draft a business succession plan that not only integrates gift and estate tax planning but also takes into account the desire to maintain family harmony for future generations.

Written by Abbie M.B. Everist. Copyright © 2024 BDO USA, P.C. All rights reserved. www.bdo.com